Liquidity is Value (Updated)

Liquidity is Value (Updated)

Matters are Worse

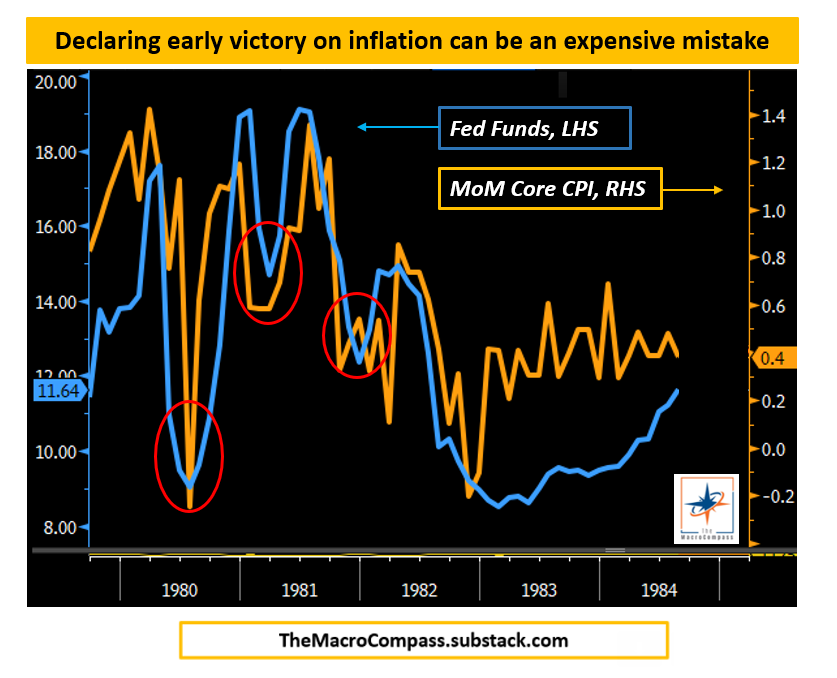

In July I wrote that we were most likely in for a grinding sideways move in valuations for all assets: real estate, stocks, bonds, and private businesses; and a continued winter for crypto and venture. After the Fed’s FOMC1 meeting yesterday, I’m updating my view. I think we are headed for a recession and I’ve become increasingly convinced that it will be a deep and painful one. I hope it is short but I’m beginning to doubt even that. The reason I think so is because of this chart from Alf at The Macro Compass:

If you aren’t a subscriber, I urge you to check his substack out. Why does this chart scare me a bit? I have to bore you with a bit of Federal Reserve history to explain.

A Story about the Federal Reserve

Once upon a time, in the 1970s, there was a Chairman of the Federal Reserve named Arthur Burns. He is mostly vilified today because he didn’t contain inflation. He repeatedly raised rates in the face of inflation and then as soon as he saw a sign that the economy was weakening, he’d cut them. But then as sure as the sun will rise, inflation started going right back up. He’d have to raise rates again and usually had to raise them higher. He was effectively chasing inflation higher. Then there were gas lines, stagflation, and people were miserable.2

After a decade in the wilderness, President Carter appointed the modern day Moses to the Fed, Paul Volcker, to guide us back to the promised land. As the story goes, he raised rates really high and kept them there for a long time until he actually got us to the promised land3. But along the way America endured 15%+ home mortgages and unemployment above 10% in the deep recession that followed his rate increases.

I’ve been told that story repeatedly by the media. As I knew it, Burns lacked conviction and it took Volcker to raise rates to 18% and keep them there until they glided down to 2% and we all live happily ever after. It sounded like a year long story. By the middle of Reagan’s first term it was Morning in America Again.

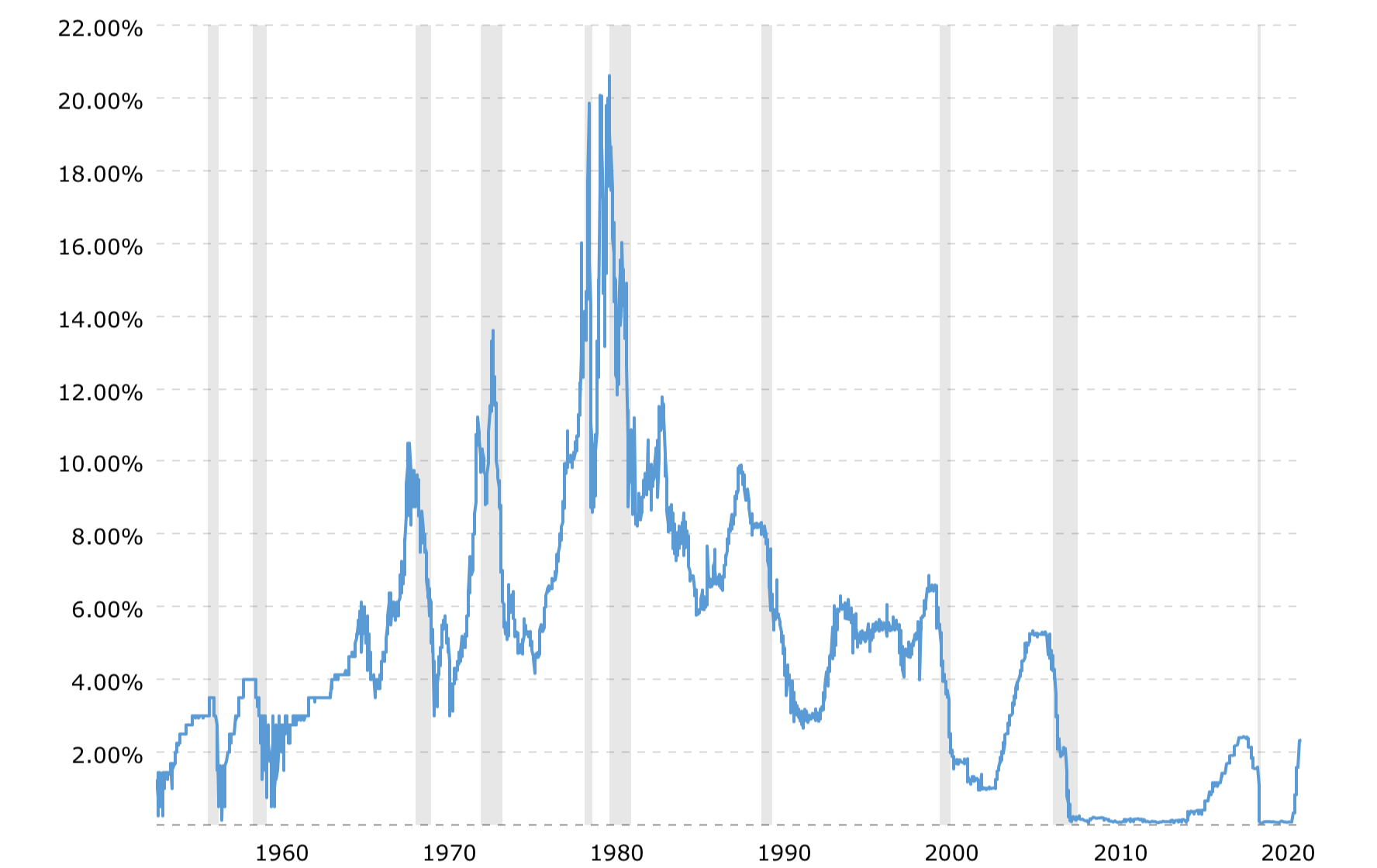

The chart above tells a very different tale. Yes, Volcker got there but it wasn’t a one and done affair. Notice that Volcker himself chased inflation higher. He cut rates twice only to raise them back higher. Interest rates didn’t get below 15% until 1982 (3 years in) and they didn’t get below 6% until 1986 (7 years in!). The unemployment rate that peaked at just under 11% didn’t get back below 6% until 1987. We even saw 10% interest rates in 1989. That’s why George HW Bush was a one termer. Here’s a much longer term chart of Fed Funds Rates from Macro Trends.

So Why is All This Stuff Important?

I think the market has been making a fundamental mistake. It’s been thinking that Jerome Powell is Arthur Burns. As we’ve seen over the summer, as soon as one price goes down a bit (like gasoline has), the NFT and meme stock speculators are back in force. We saw it with the rally in July that died after hawkish remarks made by Powell at the Fed’s Jackson Hole meeting in August. We saw it just a few days ago as the stock market crept higher before the latest Fed meeting.

If the markets believed Powell was Paul Volcker, the S&P 500 would be gapping down 2-3% or more a day4. I also think that every cash flow challenged company that rolled its debt last year at historically low rates thinks Powell is Burns. Every single family rental company that is levered to the hilt thinks Powell is Burns. Every multifamily or storage investor that bought at 4 caps thinks that Powell is Burns.

The Worm Is Turning

The stock and bond markets are starting to figure it out, and private markets are in various stages of acceptance but I predict a lot more pain ahead. Powell knew Volcker personally and frequently cites him as his mentor and model as a central banker. He’s seen both the charts above and knows that if he doesn’t raise rates high and keep them high, he (or more likely his successor) will be chasing inflation for years to come. He certainly knows that holding rates high while the economy melts down is what he has to do. I believe that at least for now his other colleagues on the FOMC are like minded.

I think they’ll keep rates high as gasoline goes down. I think they’ll keep rates high as the housing market freezes. I think they’ll keep rates high even as they see wages stop rising. And I think they’ll keep rates high even as they see unemployment spike. Those companies that refinanced last year will have to refinance again at some point. For the last 15 years just playing for time meant that you’d get lower rates on a refinance. The charts above are not encouraging for that belief system.

Rates will most likely be double or more of what a company or a person locked in last year5. To a lesser degree the same will apply for highly leveraged real estate owners with shorter term financing. But as more and more go bankrupt and fewer potential buyers want to catch a falling knife….

Can the Fed Persevere?

What Powell has to do is not an easy thing. Volcker was hated. Builders sent him 2 by 4s they couldn’t use and car dealers famously sent him the keys to the cars they couldn’t sell in coffins. He was denounced by the Treasury (where he used to work) and by Democrats and Republicans alike in Congress. I think those expressions of frustration were people getting used to prices going down. It sucks. It took that kind of pain and the anger it caused to reset expectations.

We are going to have to see the same before inflation comes down for us. So until Bored Ape owners are sending print outs of the block chain code for their NFTs to Powell’s office encased in sepulchers, I won’t believe that the back of inflation is broken. I think Powell can do it and knows he has to but there are always ways a apply pressure (a bill was introduced in Congress to impeach Volcker).

Mom (the Fed) and Dad (the Congress) are Sending You to Military School

This isn’t going to be fun going forward. Lots of people are going to lose their jobs and lots of companies are going to go bankrupt. This isn’t end of the world stuff like 2008 but it’s going to be nasty.

The big problem I see is that almost no one who isn’t retired has lived through a real recession before and for those who have, it’s a distant memory. Sure we’ve had big downturns like 2008 and 2020 but the Fed and the Federal Government came in both times and dumped tons of money to make sure the pain didn’t last long. They aren’t going to do that this time.

All parties clearly agree that the inflation we are experiencing is the result of the bailouts. Mom and Dad are making us take our medicine after 20 plus years of bailing us out. Our bedroom is being converted into an exercise area and we’re getting sent to military school to “shape up.” Add to that a probably deadlocked Congress after the mid-terms and a stubborn Fed, and “buy the dip” is going to be a thing of the past.

Implications and Recommendations

To put it simply: have lots of cash and stay patient. Last year my recommendation was take on all the debt you can. This year it’s load up the cash side of that balance sheet. In public markets I’d suggest waiting to buy until we start seeing real signs of stress. I’m not an investment advisor and don’t know much more than what I read but I think we need to see 30-40% reductions in the S&P 500 from the peak6. That’s somewhere around 3000 to 3400. That’s probably about where it should be valued but markets get crazy and it could easily overshoot those targets.

But remember private markets will be different. Because public markets are so much larger and liquid they are well ahead of private ones. Probably 12 months or more ahead. We haven’t seen the pain at all there yet beyond VC. Venture is very tied to public IPOs and companies aren’t profitable and rely heavily on fundraising on short time frames. Other parts of the private market will be much slower to respond.

I think the housing market is a pretty good example of how private markets work. What we are seeing there is a freeze. Sellers are anchored to last year’s valuations and don’t want to sell for less and buyers can’t afford those prices with mortgage rates where they are. Most sellers also locked in 30 year mortgages at those low rates so they don’t have to sell.

I could see many private markets in real estate and private equity freezing like housing. If you have a good asset and have cash flows why sell in a falling market? There is one part of those markets that is different though. Banks limit how much you can lever your house but many companies and commercial real estate lenders allow far more leverage. Those that took the most leverage for the shortest terms will start falling in the next few months. Deals that might seem good now will become available, but once the recession starts in earnest, those deals will seem less so.

I can’t tell you where or when the bottom will be but I’m going to wait a bit before pouncing on anything. Valuations will reset much like the guy in The Sun Also Rises went bankrupt: slowly at first and then all at once. Right now sellers still think Powell is Burns even if they don’t know who that is. They are anchored to the buy the dip/bailout mentality of the last 14 years. Once the realize there will be no bailout, they’ll look like Wile E Coyote realizing there is no ground beneath him. You’ll have to have the courage to buy once people start feeling like that. Wait until you see the signs of panic.

All I can say is that if Powell hangs tough, it will take a couple of years but inflation will reset. The economy will grow again and if you can pick up a few good assets during the maximum period of panic, you’ll be sitting pretty. That is no easy task. Buffett isn’t the greatest of all time because it’s easy. Good luck.

Federal Open Market Committee that sets short term interest rates.

Also the Dallas Cowboys were good. Just another sign that America was in trouble.

No analogy is perfect.

I wrote this yesterday 9/22. As of 3:45 EST on 9/23 the S&P 500 is down 1.71%.

If you think I’m smoking crack look at 30 year mortgages. They’ve more than doubled.

Another indicator I look at is the spread between high yield bonds and treasuries. It’s a measure of the risk of riskier companies over the risk free rate of treasuries. It usually spikes up to 7-10% plus right before a big downturn. You can see it here: https://fred.stlouisfed.org/series/BAMLH0A0HYM2/